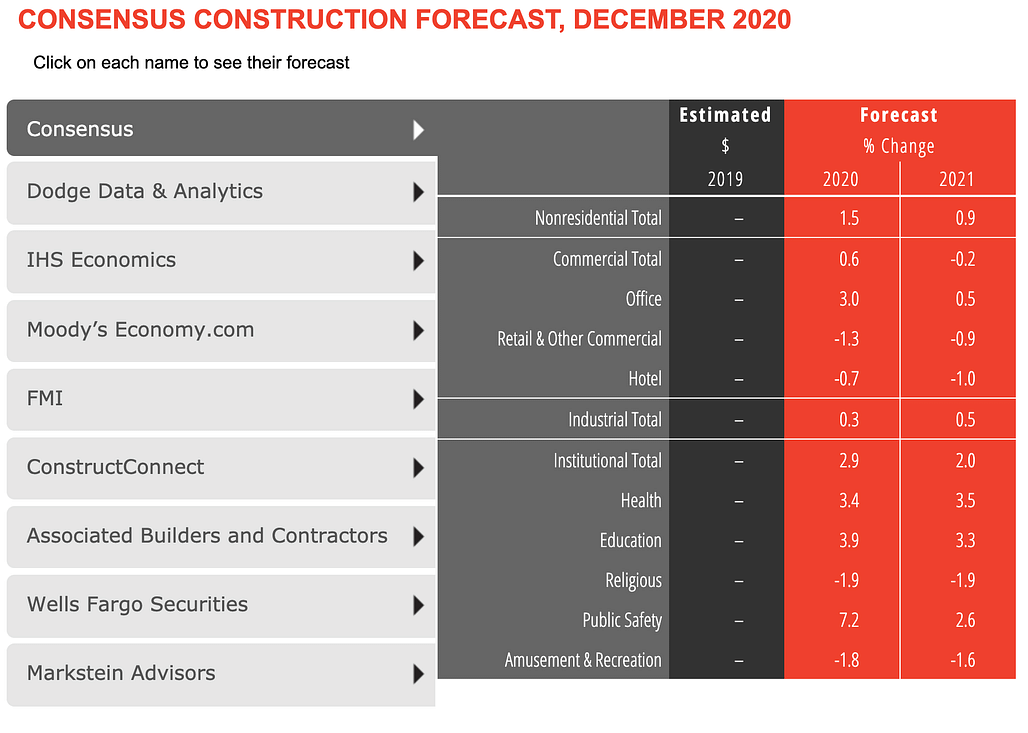

According to a recently published economic report from the American Institute of Architects (AIA), the nation's nonresidential construction sector is expected to see growth of "just 1.5 percent through 2020," with a "less than a one percent increase" projected for 2021.

The report does little to either worsen or assuage long-running fears that a recession may take hold sometime during 2020, and instead offers anemic growth projections for the coming two years.

The prognostication comes from the so-called Consensus Construction Forecast created by AIA that combines economic forecasts for different market sectors from a panel made up of leading market entities, including Moody's, Wells Fargo, and Dodge Data & Analytics.

For the coming year, the consensus forecast envisions relatively strong growth for the education (3.9%), office (3.0%) and institutional (2.9%) segments, with the strongest growth coming from so-called "public safety" projects, which are projected to grow by a whopping 7.2%. These sectors are all expected to show continued, though much more tepid, growth in 2021.

The religious (-1.9%), amusement (-1.8%), retail (-1.3%), and hotel (-0.7%) markets are expected to contract over the next two years as ongoing slow-downs in certain segments of the commercial construction industry continue on their downward march.

The brief but cautious report represents a slight upgrade in terms of mood from what was presented in mid-2019, when the AIA's Chief Economist, Kermit Baker, wrote that "downside risks continue to outweigh upside opportunities" with regards to the economic picture heading into 2020.

At the time, the US was deep into a trade tariff dispute with China that had just begun to be felt by the nation's industrial and business sectors, and firms had racked up a series of disappointing Architecture Billings Index (ABI) reports.

Six months later, those trade tensions have dissipated somewhat, though not entirely, while other sectors of the construction industry, namely residential construction, have shown marked growth. Architecture billings rallied for the last three months of the year, ending 2019 on a positive note following a depressed summer and fall.

With regards to nationwide recession worries, the picture remains somewhat mixed, as the three leading indicators—unemployment rates, US Treasury bonds, and manufacturing strength—are pointing in different directions. The national unemployment rate has remained at historic lows, between 3.5% and 3.7% since April 2019, which is good. Meanwhile, however, the interest rates on United States Treasury short term yields have fluctuated between typical and "inverted" figures—not bad, but also not so good—and the manufacturing industry has struggled to recover from the summer trade woes—not good. To boot, new worries about the expected spread of the deadly coronavirus in China have created a deep well of uncertainty for the "biggest driver of global growth," according to recent reports.

Simply put, for the architecture industry, the economic picture has remained unchanged from Baker's 2019 prognostications of meager-to-decent short-term growth and largely unpredictable, but likely not catastrophic, economic conditions further down the road.

As far as architecture firms are concerned, Baker reports: “The broader economy is expected to continue to see slower growth this year, but the number of potential trouble spots seems to be diminishing. Revenue trends at architecture firms saw an uptick in the fourth quarter last year, which suggests construction spending will continue to see growth in the coming quarters.”

No Comments

Block this user

Are you sure you want to block this user and hide all related comments throughout the site?

Archinect

This is your first comment on Archinect. Your comment will be visible once approved.