Welcome to the sixth installment of Archinect's series, State of AEC. At the end of each month, we will guide you through the latest analyses, indexes, and trends on how the architecture and construction industries are performing economically.

Throughout the past month, several key indicators related to architectural business have either stabilized or turned positive, counteracting a year of largely negative numbers. The AIA's Architecture Billings Index marginally turned positive for the first time in almost two years, while billings also increased in firms located in the South region and in firms specializing in institutional projects. For some commentators, such numbers are the early shoots of a more positive economic landscape expected in 2025.

Read our full roundup of the month's economic and business figures below and find out more about how the business health of the architecture profession is faring via our recently released survey results here.

Design and Planning

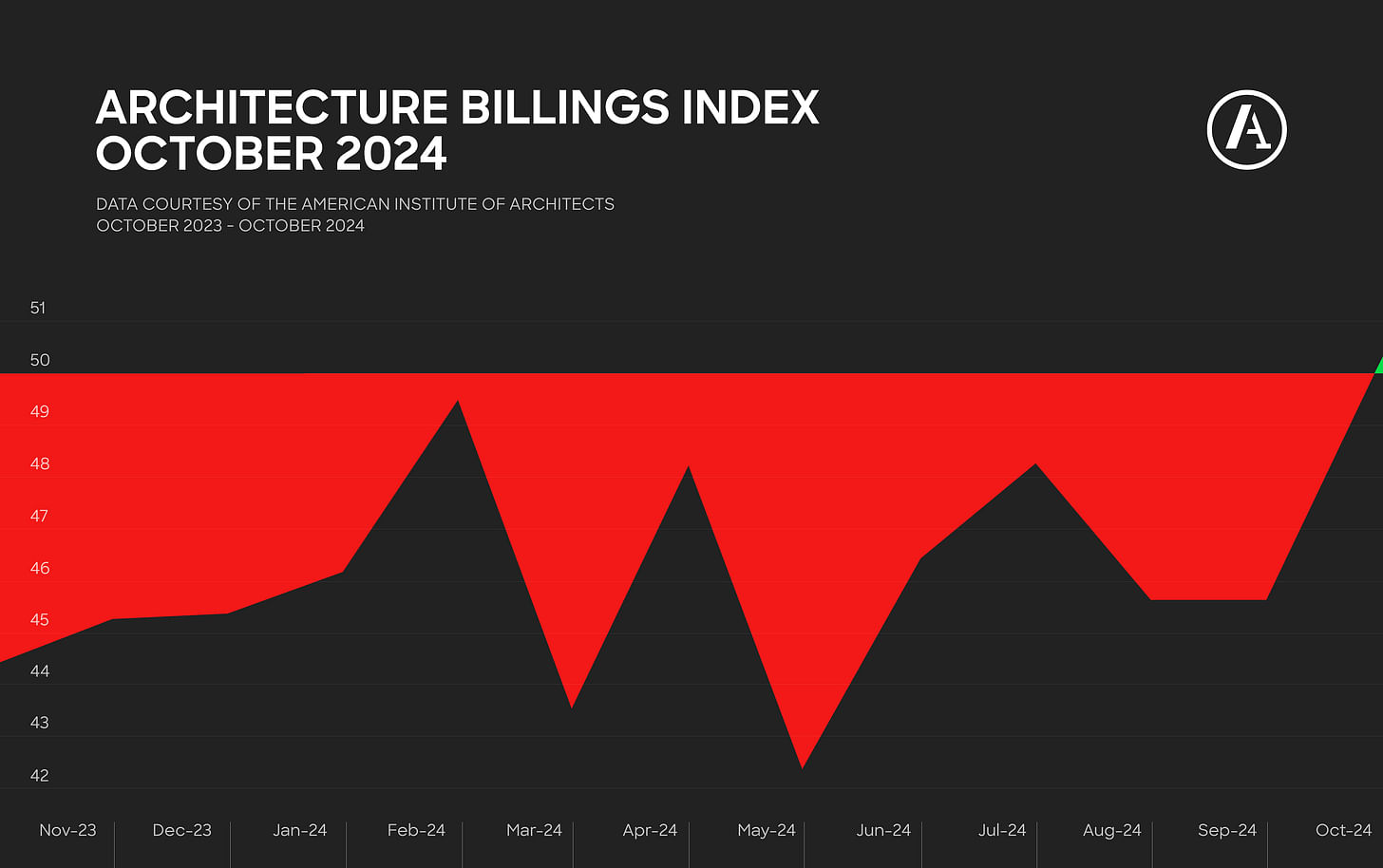

The latest AIA/Deltek Architecture Billings Index (ABI), covering October, found that billings have stabilized at architecture firms versus the previous months for the first time in almost two years. The index score of 50.3 indicates that marginally more firms reported an increase in billings in the previous month than reported a decrease.

While billings remained steady, firms are continuing to see an increase in new inquiries, as they have done for the past year. The value of new contracts signed has decreased, however, with marginally more architecture firms saying that contract values declined last month. The rate of decline in new design contracts has accelerated, reversing a slowing decline over the past five months.

"Billings finally stabilized this month, and firms are feeling more optimistic about revenue projections for 2025," said the AIA's Chief Economist, Kermit Baker. "Overall, 41 percent of responding firm leaders expect to see net revenue growth from 2024 to 2025, with 32 percent projecting growth in the 5 percent to 9 percent range."

Baker’s note that firms are more optimistic about 2025 revenue projects comes amid two interest rate cuts by the Federal Reserve in recent months, with another cut predicted before 2024 ends. You can read more about the relationship between interest rate cuts and architecture service demands in our recent feature article on the subject.

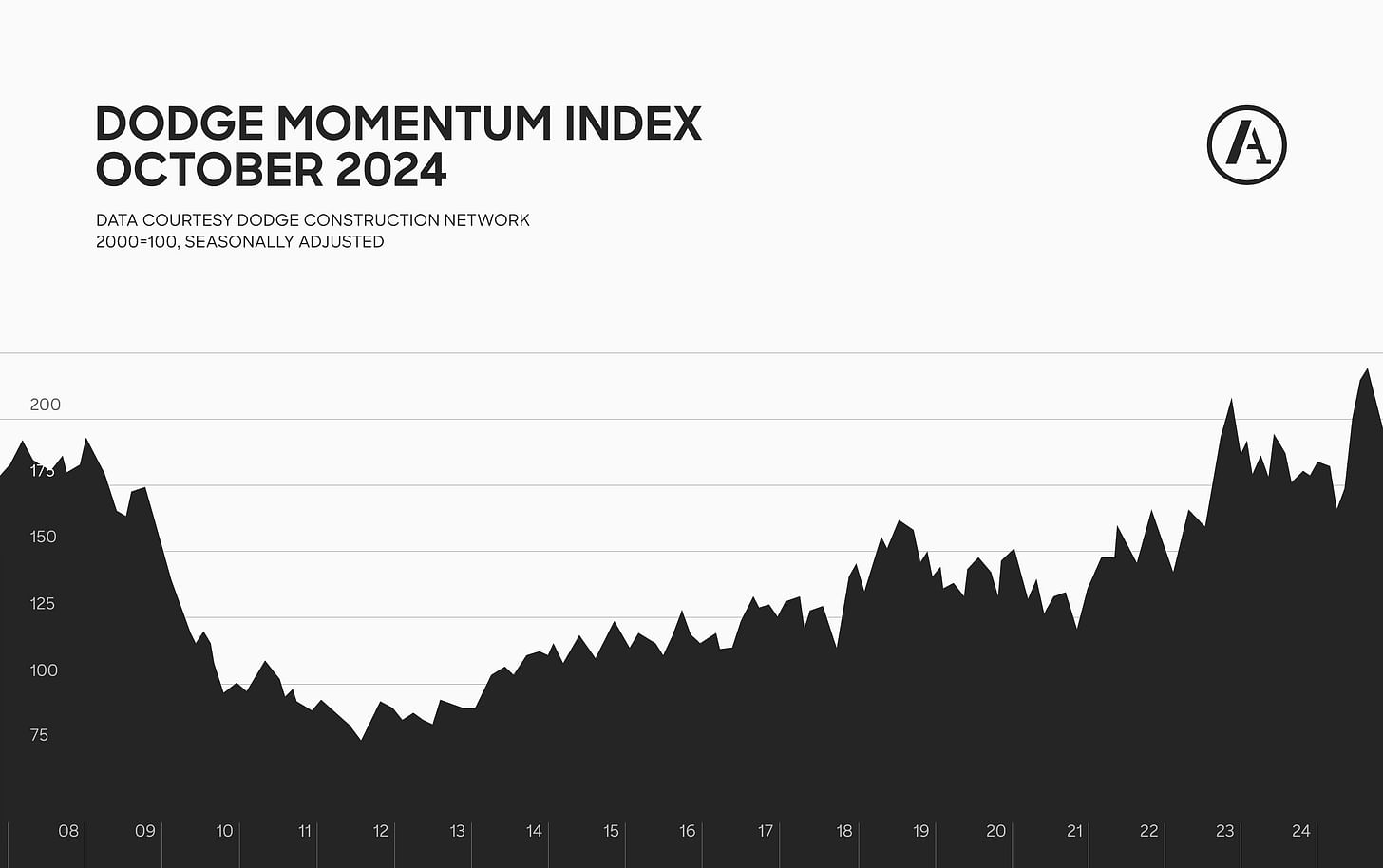

Elsewhere, October's Dodge Momentum Index, which measures the value of nonresidential building projects going into planning, saw a 5.3% decrease from the previous month. Despite the drop, the index remains at a near-high figure from recent years and sits 13% higher than in October 2023.

"In addition to data center planning normalizing, a moderate pullback in the number of planning projects for several other nonresidential sectors also contributed to the decline in the Dodge Momentum Index for October," Sarah Martin, the Associate Director of Forecasting at Dodge Construction Network, said. "Regardless, owners and developers remain confident in next year’s market conditions, and the planning queue remains poised to spur stronger construction activity in 2025, following deeper rate cuts by the Fed."

Construction

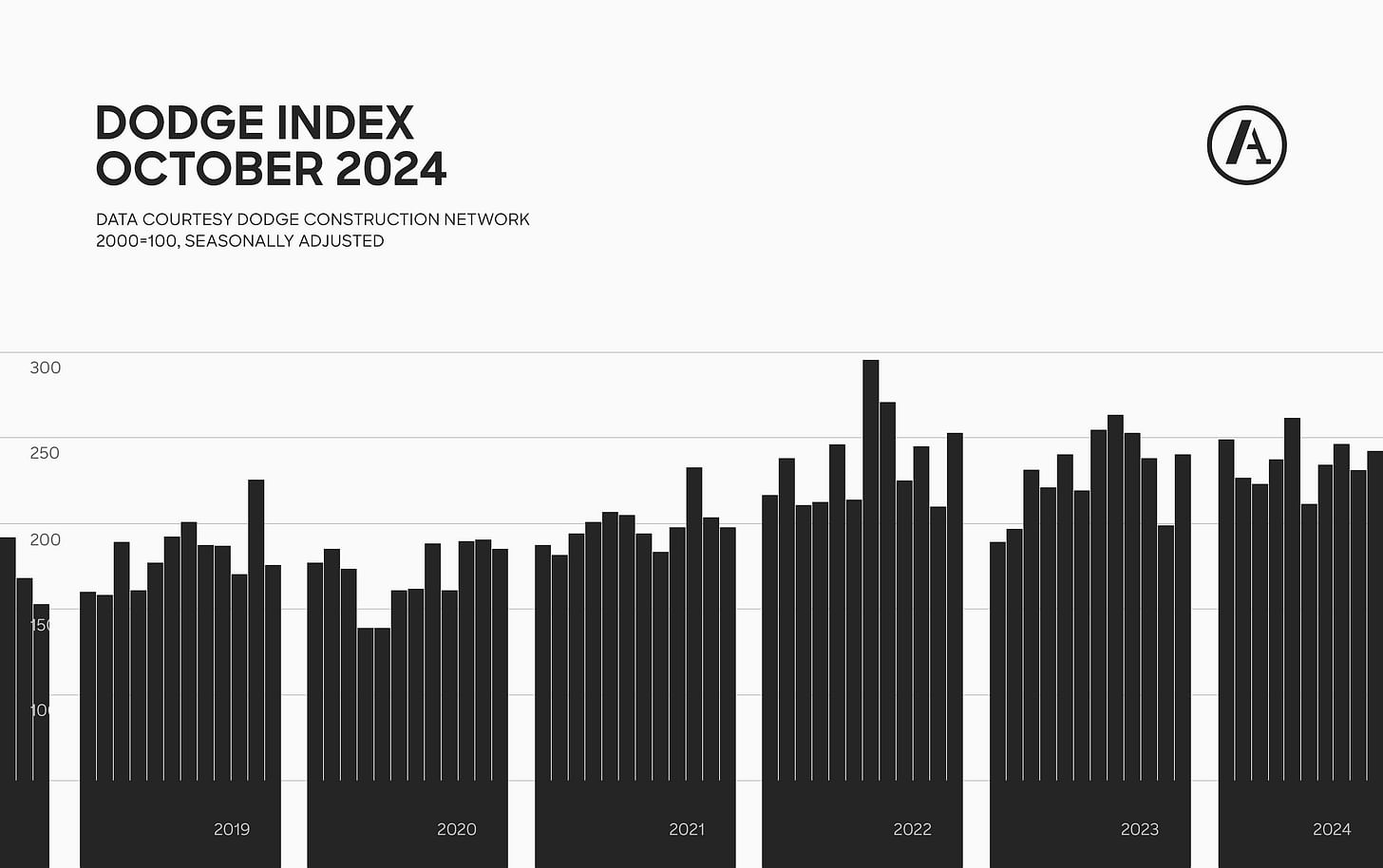

Overall, total construction starts across the United States rose 4% last month, according to Dodge Construction Network. For the 12 months ending in October 2024, total construction starts are up 3% from the 12 months ending October 2023.

"Construction starts have yet to see the impact of falling interest rates," said Dodge Construction Network Chief Economist Richard Branch. "Several more rate cuts will be needed to start moving construction projects through the planning process to start. Clarity, though, has improved now that the election is in the rearview mirror; however, developers may wait until the full scope of President-elect Trump’s legislative agenda comes into better focus."

While construction activity rose last month, so did the cost of producing materials for construction. Data from the U.S. Bureau of Labor Statistics showed that construction input prices increased by 0.3%, including a 0.5% increase in softwood lumber and a 0.6% increase in concrete products.

"Higher energy prices drove the increase in construction input prices observed in October," said ABC Chief Economist Anirban Basu. "While prices for a few other materials, like concrete and copper products, also rose for the month, overall input prices are lower than they were one year ago and have fallen 5% since reaching an all-time high in June 2022."

Elsewhere, project delays, pauses, and abandonments in the non-residential sector experienced a marginal deterioration last month. ConstructConnect’s latest Project Stress Index saw a 0.8% increase in its October metric compared to September. ConstructConnect notes in their analysis that abandonments and pauses have declined this year in part due to Fed interest rate cuts.

Northeast

Architecture firms in the Northeast told the AIA ABI that business conditions have deteriorated, with September’s 45.6 score showing a decline in billings on the previous months. Poor performance in August, September, and October follows three months of billings in the Northeast sitting in or around 50 points — the first showing in positive territory for a year.

Total construction starts in the Northeast increased last month, according to Dodge Construction Network, while U.S. Census data shows that residential unit permits granted increased by 12% on last month though decreased 7% on October 2023, seasonally adjusted.

Midwest

According to the ABI, business conditions in architecture firms in the Midwest are in decline. While such firms have reported declines every month this year, October's score of 46.9 is the highest score the Midwest has posted in the ABI since February 2024.

Total construction starts in the Midwest increased last month, according to Dodge Construction Network, while U.S. Census data shows that residential unit permits granted decreased by 2% on last month but increased 13% on October 2023, seasonally adjusted.

West

Firms in the West region have seen a continuing decline in business conditions in the ABI. The latest ABI score of 47.6 is nonetheless the highest score posted by the West since March 2024. The West continues to see the longest duration of decline of any region, at 25 consecutive months.

Total construction starts in the West also decreased last month, according to Dodge Construction Network, while U.S. Census data shows that residential unit permits granted decreased by 2% on last month and decreased by 6% on October 2023, seasonally adjusted.

South

Firms in the South region were the only U.S. region to see growth in October, with a score of 52.1 meaning marginally more firms saw an increase in billings versus September than saw a decrease. For the past three months, the South has been the strongest-performing region in the ABI.

Total construction starts in the South fell last month, according to Dodge Construction Network, while U.S. Census data shows that residential unit permits granted decreased by 1% on last month and fell 12% on October 2023, seasonally adjusted.

Residential

According to the ABI, firms specializing in multifamily residential projects have continued to see a decline in billings. Such firms have not reported an increase in billings from the previous month since August 2022.

On the construction side, the number of residential starts fell by 3%, according to Dodge Construction Network. For the 12 months ending October 2024, residential construction starts were up 7% from the 12 months ending October 2023.

Digging deeper into the residential sector, single-family starts fell by 4%, according to Dodge, while multifamily starts fell by 2%. Over the past twelve months, single-family starts have risen 17% versus the previous twelve-month period, although multifamily starts were 9% lower.

Commercial/Industrial

Firms specializing in major non-residential sectors have reported a decline in billings in the previous month. According to the ABI, firms specializing in commercial/industrial projects continue to see a deterioration in billings, though not as severely as the previous month. The last time such firms reported an increase in billings in the previous month was July 2023.

In addition to a decline in billings for commercial projects, the value of commercial projects currently in planning has declined by 6.7% on last month, according to the Dodge Momentum Index, though the value of such projects was up 18% on this time last year.

In construction, commercial starts are up 3% on last month. Meanwhile, manufacturing project starts increased 114% from September due to the start of several major projects. For the 12 months ending in October 2024, commercial starts are down 1% more than the previous 12 months, with industrial starts being down 33%.

Institutional/Cultural

Firms specializing in institutional projects reported an increase in billings last month, according to the ABI. This marks the first increase in billings seen in the sector since July 2023.

Despite a decline in billings, there has been an increase in the value of institutional projects currently being planned. The Dodge Momentum Index reports that the value of planned institutional projects has declined 2%, while the value of such projects is up 3% on this time last year.

In construction, institutional starts rose 13% in October, according to Dodge Construction Network, while for the 12 months ending in October 2024, institutional starts are up 16% from the previous 12 months.

"It is not surprising that optimal hiring is often when the firm enters a new cycle of projects and can develop existing staff and bring in new talent to forge a strong team," Marvel partners Lissa So and Annya Ramirez told Archinect in a recent feature on when firms should start hiring. "Knowing that things are always unpredictable, hiring requires reading into the future and a bit of luck."

"There is still a lot of ‘wait and see,’ but there is a lot more positive conversation than negative, and we feel poised to have a strong 2025," a 45-person firm in the South specializing in commercial/industrial projects told the AIA ABI, meanwhile.

"Bonds for affordable housing have not been passing, so there’s a lot of concern about the viability of nonprofit housing developers remaining in business due to lack of funding for projects," a 12-person firm in the West with a residential specialization added.

Niall Patrick Walsh is an architect and journalist, living in Belfast, Ireland. He writes feature articles for Archinect and leads the Archinect In-Depth series. He is also a licensed architect in the UK and Ireland, having previously worked at BDP, one of the largest design + ...

No Comments

Block this user

Are you sure you want to block this user and hide all related comments throughout the site?

Archinect

This is your first comment on Archinect. Your comment will be visible once approved.