Welcome to the fifth installment of Archinect's new series, State of AEC. At the end of each month, we will guide you through the latest analyses, indexes, and trends on how the architecture and construction industries are performing economically.

Throughout the last month, commentators in the architecture and planning spheres have noted that, although interest rates were cut in September, clients remain cautious about commissioning architects for new projects or committing projects to planning. For one commentator, the industry may not feel the full positive impact of the rate cuts until the middle of 2025, which may lead to strong nonresidential planning performance.

Read our full roundup of the month's economic and business figures below and find out more about how the business health of the architecture profession is faring via our recently released survey results here.

Design and Planning

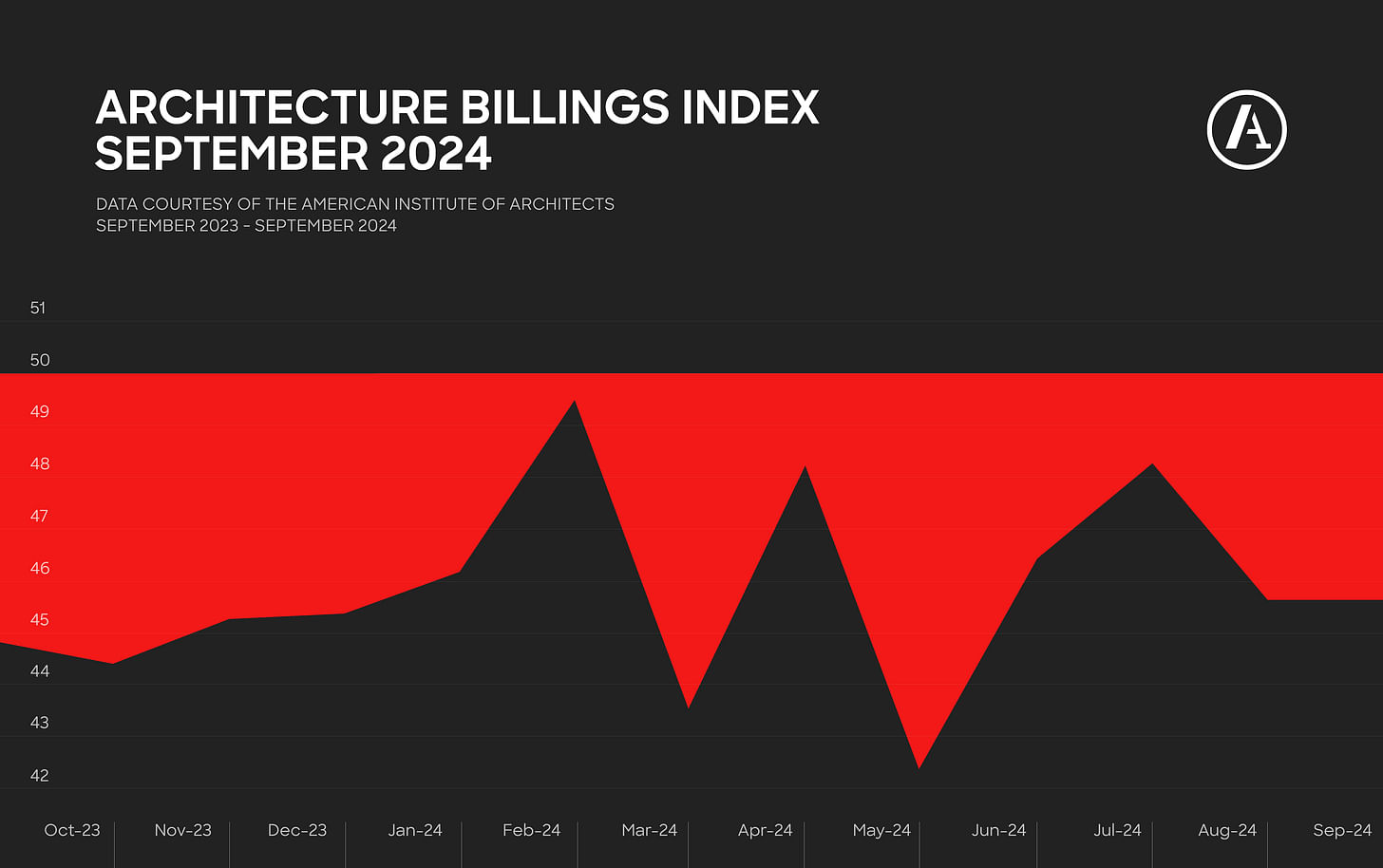

The latest AIA/Deltek Architecture Billings Index (ABI), covering September, found that billings are continuing to decline at a majority of firms and at a similar rate to the month before. The index score of 45.7 indicates that more firms reported a decline in billings in the previous month than reported an increase.

While billings declined, firms are continuing to see an increase in new inquiries, as they have done for the past year. The dollar value of new contracts signed has decreased, however, with marginally more architecture firms saying that contract values declined last month. The rate of decline in new design contracts has slowed since August.

“Despite recently announced rate cuts by the Federal Reserve, clients are still cautious about future projects,” the AIA notes about the latest figures. “Inquiries into potential new projects continued to increase, but the pace has slowed since the beginning of the year. And the value of newly signed design contracts at firms decreased for the sixth consecutive month in September, although the pace of that decline has moderated somewhat over the last few months.”

AIA’s assertion that a recent Federal Reserve interest rate cut has not immediately translated into industry growth aligns with our recent feature article analyzing what the move means for architects. Our summary findings were that although the rate cuts will have a positive impact on architectural business conditions, it may be several months before such an impact is felt.

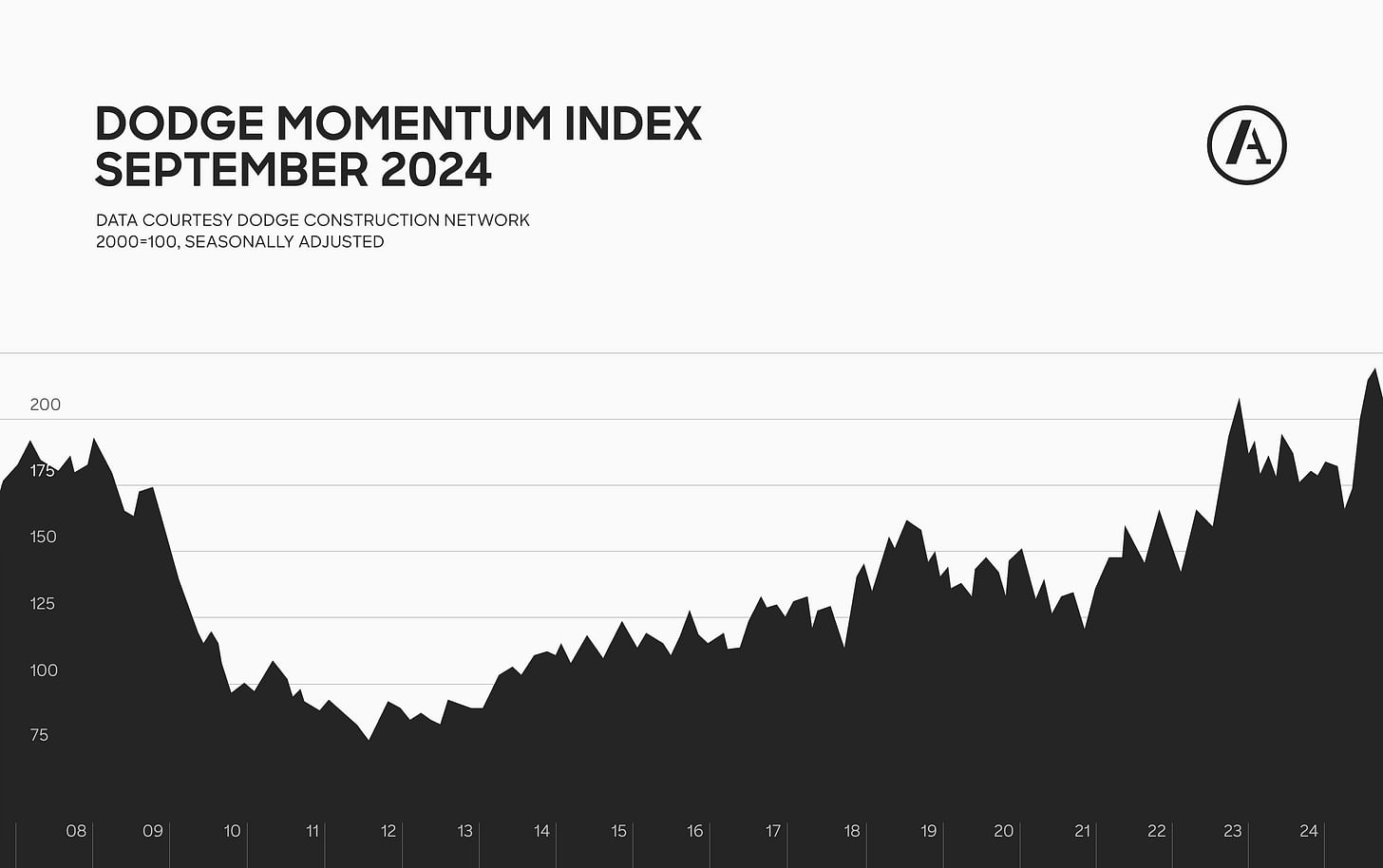

Elsewhere, September's Dodge Momentum Index, which measures the value of nonresidential building projects going into planning, saw a 4% decrease from the previous month. Despite the drop, the index remains at a near-high figure from recent years and sits 21% higher than in September 2023.

“Despite this month’s decline, the Dodge Momentum Index remains at very robust levels,” Sarah Martin, the Associate Director of Forecasting at Dodge Construction Network, said. “A surge in data center activity drove much of the recent rapid growth in the DMI — so as planning for that sector moderated over the month, overall commercial planning fell back. By mid-2025, the Fed’s rate cuts should spur planning projects to reach groundbreaking more quickly — leading to stronger nonresidential activity as 2025 progresses.”

Construction

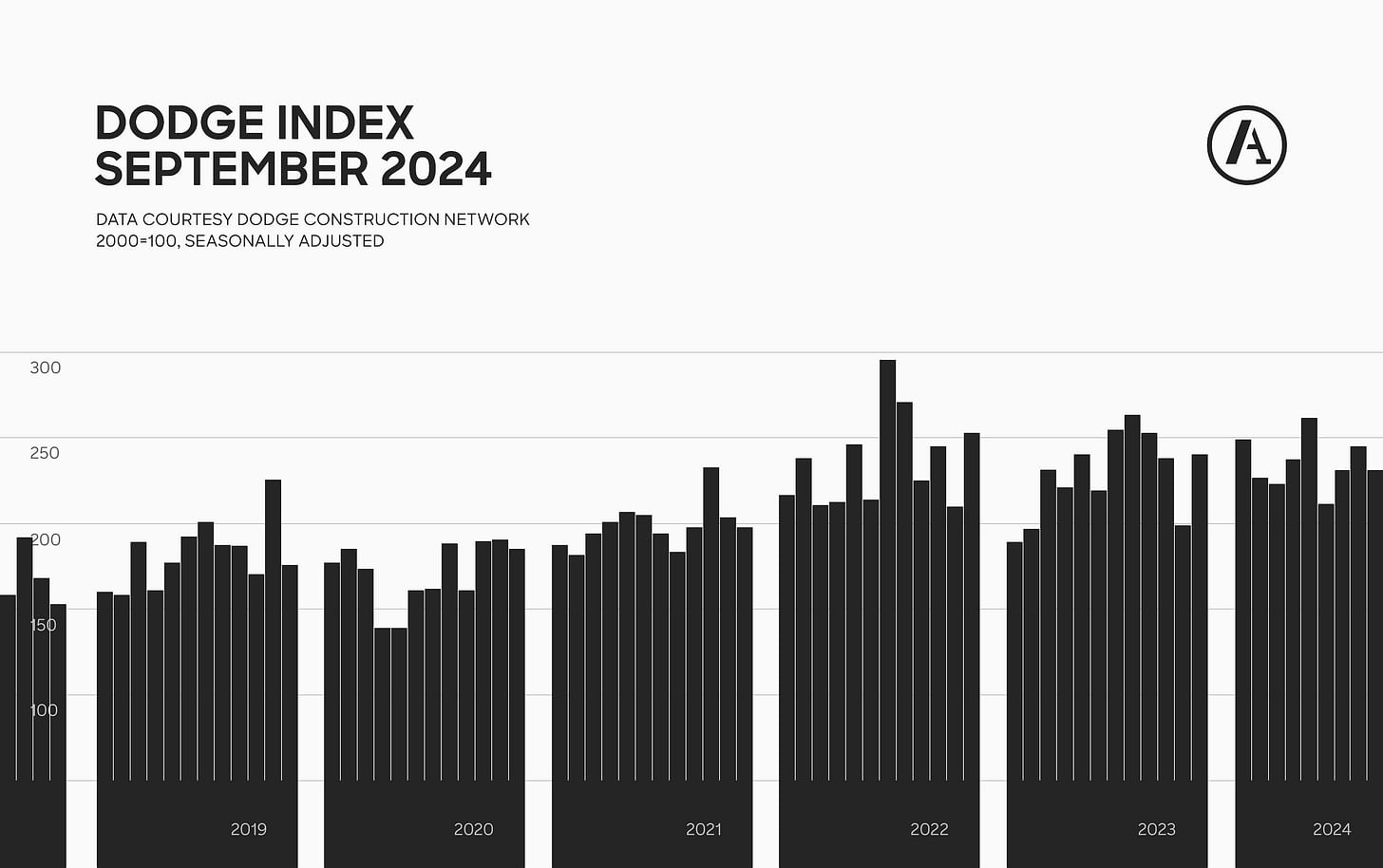

Overall, total construction starts across the United States fell 6% last month, according to Dodge Construction Network. For the 12 months ending September 2024, total construction starts are nonetheless up 2% from the 12 months ending September 2023.

“Construction starts are treading water,” Dodge Chief Economist Richard Branch said. “September’s rate cut was just the first step in unwinding a period of high rates, and several more cuts will be needed to start moving construction projects through the planning process. More consistent growth in construction starts should begin to materialize early in the new year.”

While construction activity fell last month, so did the cost of producing materials for construction. Data from the U.S. Bureau of Labor Statistics showed that construction input prices decreased by 0.9%, despite a 2.5% increase in softwood lumber and a marginal 0.3% increase in concrete products.

“The decline in construction input costs observed in September was almost entirely due to a large decrease in oil prices,” Associated Builders and Contractors Chief Economist Anirban Basu said. “While domestic freight rates are low by historical standards, elevated global container-shipping rates and emerging supply chain issues could put upward pressure on materials prices in the coming months. This represents a cause for concern for contractors, many of whom expect their profit margins to contract over the next six months, according to ABC’s Construction Confidence Index.”

Elsewhere, project delays, pauses, and abandonments in the non-residential sector experienced a significant increase last month. ConstructConnect’s latest Project Stress Index saw a 16.7% increase in its September metric compared to August. ConstructConnect attributes this rise in part to a downward revision of the August reading, noting that disruption is 11.7% down on September 2023.

Northeast

Architecture firms in the Northeast told the AIA ABI that business conditions have deteriorated, with September showing a decline in billings on the previous months. Poor performance in August and September follows three months of billings in the Northeast sitting in or around 50 points; the first showing in positive territory for a year.

Total construction starts in the Northeast decreased last month, according to Dodge Construction Network, while U.S. Census data shows that residential unit permits granted decreased by 13% on last month and 2% on September 2023, seasonally adjusted.

Midwest

According to the ABI, business conditions in architecture firms in the Midwest are in decline, and at a larger rate of decline than in August. While such firms have reported declines every month this year, September’s score of 45.0 ends a five-month trend of the rate of decline in billings slowing month-on-month.

Total construction starts in the Midwest decreased last month, according to Dodge Construction Network, while U.S. Census data shows that residential unit permits granted decreased by 3% on last month but increased 1% on September 2023, seasonally adjusted.

West

Firms in the West region have seen a continuing decline in business conditions in the ABI. The West has been the poorest performing U.S. region for billing trends consistently for the past three months and continues to see the longest duration of decline of any region, at 24 consecutive months.

Total construction starts in the West also decreased last month, according to Dodge Construction Network, while U.S. Census data shows that residential unit permits granted increased by 9% on last month, though decreased by 5% on September 2023, seasonally adjusted.

South

Firms in the South region have continued a 15-month trend of reporting that business conditions have worsened in the previous month, according to the ABI, though the rate of decline has slowed. At a score of 49.5, the South displays the strongest business conditions of any region.

Total construction starts in the South also increased last month, according to Dodge Construction Network, while U.S. Census data shows that residential unit permits granted decreased by 6% on last month and fell 9% on September 2023, seasonally adjusted.

Residential

According to the ABI, firms specializing in multifamily residential projects have continued to see a decline in billings. Such firms have not reported an increase in billings from the previous month since August 2022.

On the construction side, the number of residential starts rose by 7%, according to Dodge Construction Network. For the 12 months ending September 2024, residential construction starts were up 6% from the 12 months ending September 2023.

Digging deeper into the residential sector, single-family starts rose by 2%, according to Dodge, while multifamily starts fell by 6%. Over the past twelve months, single-family starts have risen 17% versus the previous twelve-month period, although multifamily starts were 10% lower.

Commercial/Industrial

Firms specializing in major non-residential sectors have reported a decline in billings in the previous month. According to the ABI, firms specializing in commercial/industrial projects continue to see a deterioration in billings, though not as severely as the previous month. The last time such firms reported an increase in billings in the previous month was July 2023.

In addition to a decline in billings for commercial projects, the value of commercial projects currently in planning has declined by 7.8% on last month, according to the Dodge Momentum Index, though the value of such projects was up 31% on this time last year.

In construction, commercial starts are up 9% on last month. Meanwhile, industrial project starts declined 30% from August. For the 12 months ending in September 2024, commercial starts are down 8% more than the previous 12 months, with industrial starts being down 17%.

Institutional/Cultural

Firms specializing in institutional projects continue to report a decline in billings, according to the ABI. Such firms have nonetheless reported a decline in billings almost every month since July 2023, with the sole exception of January 2024, where billings were stagnant on the previous month.

Despite a decline in billings, there has been an increase in the value of institutional projects currently being planned. The Dodge Momentum Index reports that the value of planned institutional projects has increased 5.2%, while the value of such projects is up 4% on this time last year.

In construction, institutional starts rose 10% in September, according to Dodge Construction Network, while for the 12 months ending in September 2024, institutional starts are up 13% from the previous 12 months.

“Once a week, make an excuse to reach out to the client, whether an email invitation to have a coffee or to go to a local restaurant,” former HOK CEO Patrick MacLeamy told me in a recent conversation on how architects can navigate through economic downturns. “Maybe they need some advanced planning on a project that is five years out. You will only know if you ask them and talk to them. Hanging onto the client is key.”

“Communicate [with staff] every day,” MacLeamy added. “Get everybody in the office together and have a simple talk. Tell them where the firm is, what the status of projects are, and what your plan is to navigate the downturn.”

“Just can’t seem to get the dam to break on getting new agreements signed for the larger projects,” a large commercial/industrial specialty firm in the West told the AIA, meanwhile. “We are hopeful that the interest rate cuts will begin to allow more projects to be greenlighted.”

Share your own experiences of the AEC sector in the comments section below. When doing so, please tell us which U.S. Census region you are based in (Northeast/Midwest/West/South) and the size of your firm.

Niall Patrick Walsh is an architect and journalist, living in Belfast, Ireland. He writes feature articles for Archinect and leads the Archinect In-Depth series. He is also a licensed architect in the UK and Ireland, having previously worked at BDP, one of the largest design + ...

No Comments

Block this user

Are you sure you want to block this user and hide all related comments throughout the site?

Archinect

This is your first comment on Archinect. Your comment will be visible once approved.