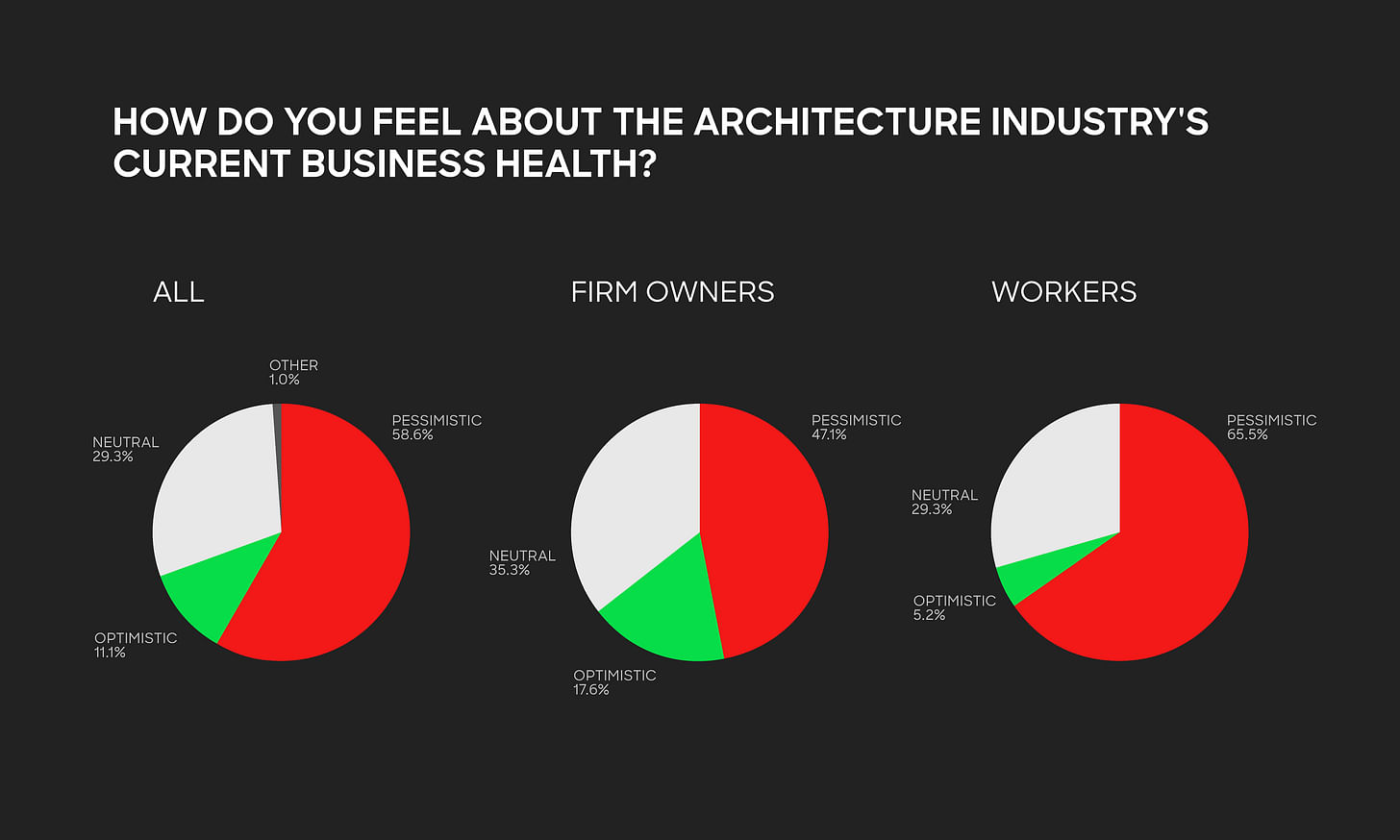

Earlier this week, we released Part One of our findings from the Archinect Business Survey, which invited you to share how you were feeling about the economic outlook of your firm and sector. Our analysis found that across the United States, architects have seen business conditions decline in the past year and are downbeat about their firm’s business health, the health of the architecture industry at large, and the wider U.S. economy. Meanwhile, clients are cautious about starting or continuing projects.

While Part One offered an insight into how architects and clients are faring within the architecture industry’s current economic slowdown, this article, Part Two, explores the potential causes of the slowdown itself. The five factors set out below reflect what respondents to our survey, and economists and commentators from within and beyond the architecture industry, have identified as driving forces behind today’s business climate.

While each of these factors deserves to be isolated and examined in its own right, it is important to note that, in real terms, these factors do not exist in vacuums. The overall picture painted from this analysis is of an architecture industry grappling with five distinct though interconnected factors, combining and feeding off each other in a unique 'perfect storm' to suppress the demand for architectural services while increasing the cost of running a practice.

The bottom line: High interest rates are discouraging clients from taking out loans for new projects, lowering the demand for architectural services.

Of all the explanations put forward by our survey respondents for the architecture industry’s economic slowdown, “high interest rates” was by far the most common. For context, the United States Federal Reserve has steadily increased its benchmark interest rate from 0.25% in March 2022, where it had sat for two years, to 5.5% by July 2023, where it remains today. The interest rate rises began after the tail end of the COVID-19 pandemic saw a surge in inflation.

While today’s 5.5% rate is the highest in two decades, it is also worth noting that the previous 0.25% rate, which the Federal Reserve maintained for much of the last fifteen years, was an all-time historical low. Nonetheless, recent days have seen the Federal Reserve express satisfaction with the “disinflationary path” taken by the U.S. leading to speculation that interest rates may be cut in September 2024.

High interest rates have taken the bottom out of residential lending, both for new mortgages and construction loans. — Archinect survey respondent

In the meantime, many respondents to our survey reported that the current interest rate level is deterring clients from borrowing money to fund construction projects, with knock-on consequences for design activity. “Many owners/developers are simply waiting for interest rates to finally come down,” an architect from a small firm in Oakland, CA, told us, while another from a medium-sized firm in New York City noted that: “High interest rates have taken the bottom out of residential lending, both for new mortgages and construction loans.”

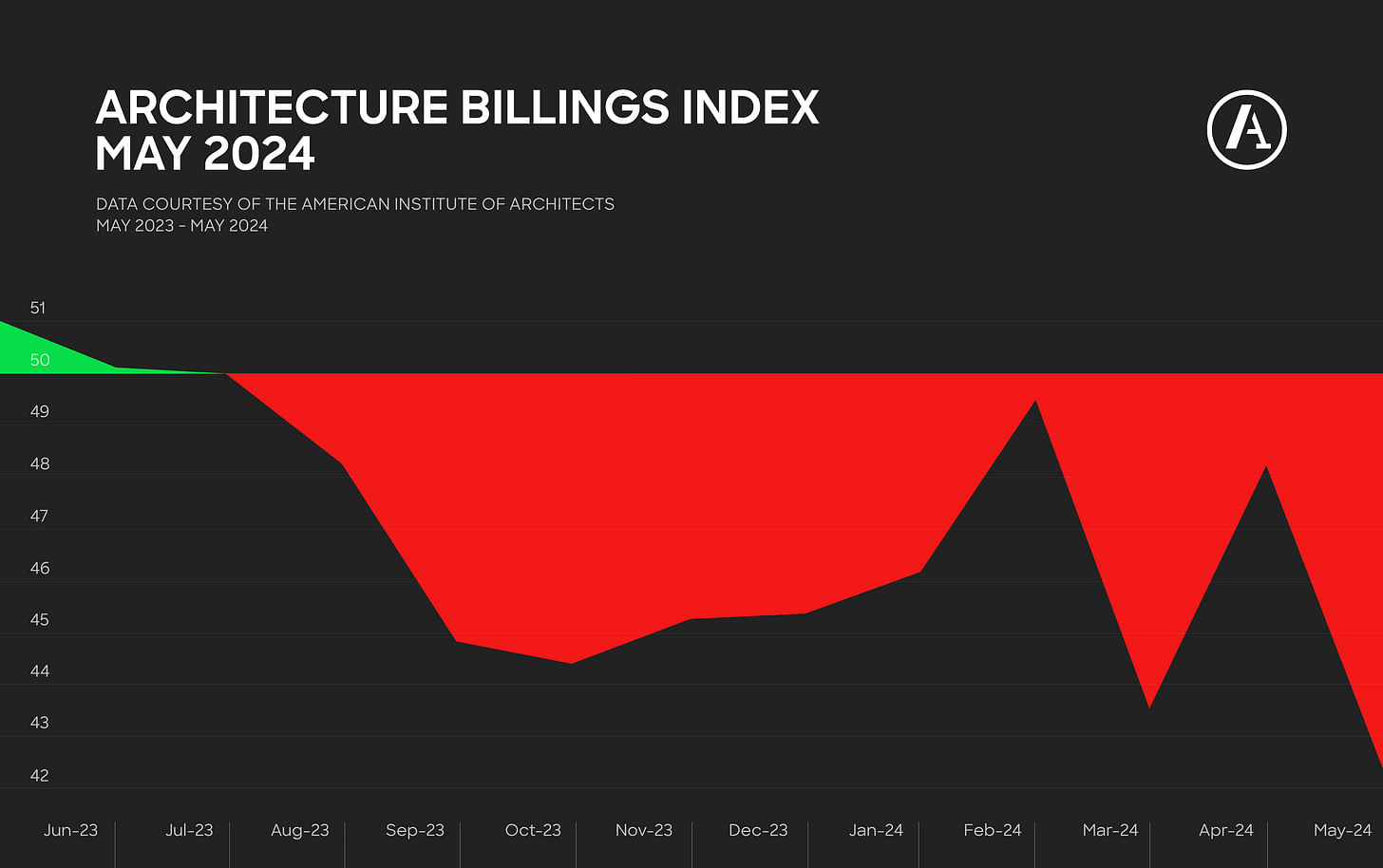

The role of interest rates was also cited by the AIA in a recent edition of the institute’s Architecture Billings Index, which has seen almost one year of consistent declines in architecture billings. “Firms had hoped that the Federal Reserve would start lowering interest rates this spring and that would open new work, but with that decrease now likely on hold until late summer or early fall, firms may have some more slow months ahead of them,” the AIA said in May.

The bottom line: Inflated material and labor expenses, and years of strong demand, are keeping the cost of construction high, discouraging clients from engaging architects on new projects.

While high interest rates have raised the cost of borrowing for construction projects, the cost of construction itself has also risen. Throughout the COVID-19 pandemic, the cost of construction materials rapidly accelerated in response to supply chain disruption. Although the rate of change has stabilized for the past year, a recent analysis by the Associated Builders and Contractors shows that the price of inputs to construction is still 41% higher than it was in February 2020. There are no signs that such prices will return to their pre-COVID levels.

In addition to high material prices, the construction industry also continues to grapple with increasing labor costs, with construction companies competing for a shrinking number of skilled workers, thus driving wages, and resulting construction costs, up. A recent analysis by the CBRE attributes this lack of skilled workers to an “aging workforce and a lack of interest in trade careers among younger generations.”

Construction costs are exceeding even the most pragmatic estimates. — Archinect survey respondent

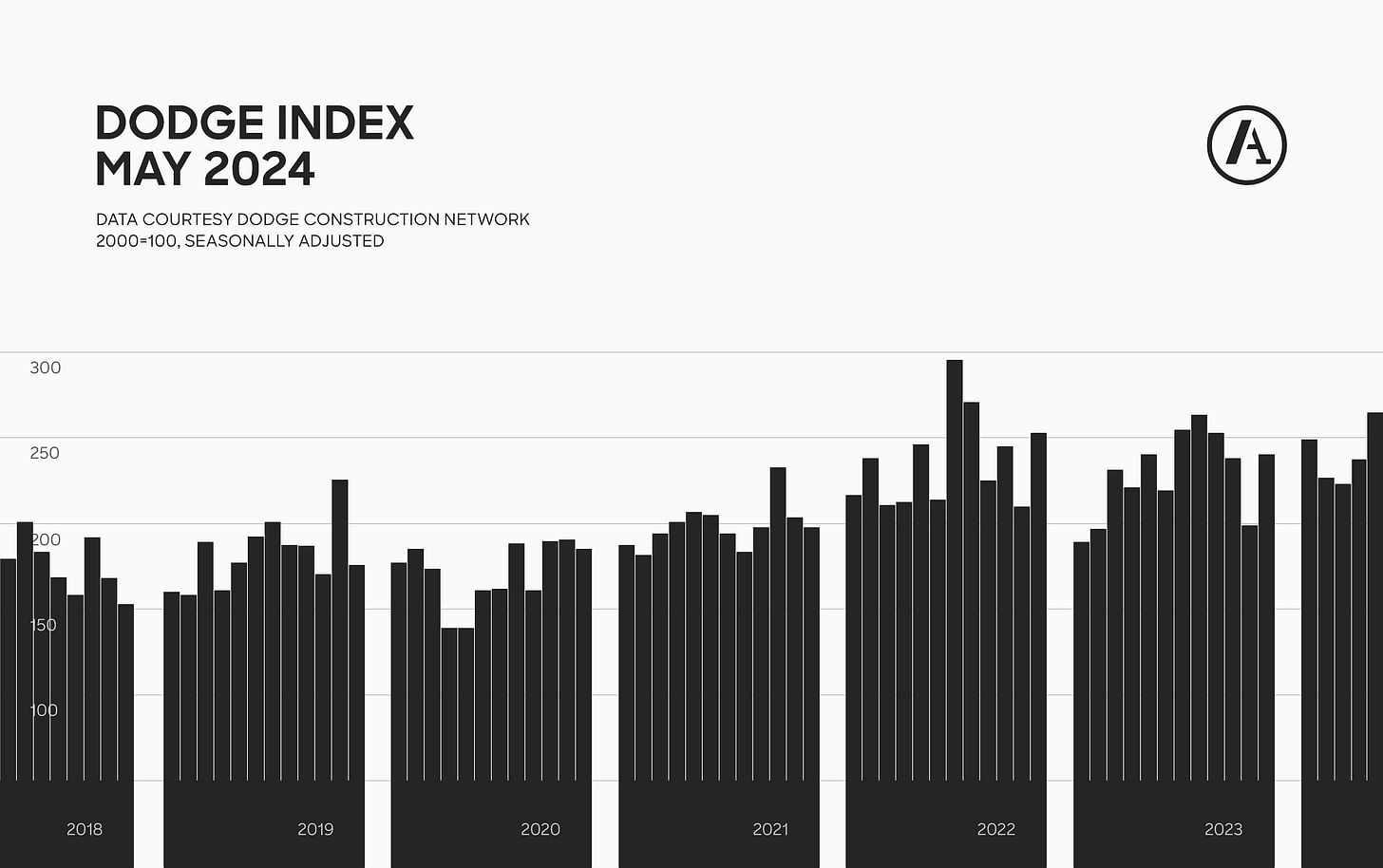

While higher material and labor costs are the most cited reasons for rising construction costs, other factors are also at play. Following the subsiding of the pandemic, the demand for construction increased significantly, as Archinect’s graphing of the Dodge Construction Starts Index shows. As the Commercial Real Estate Development Association noted in a recent analysis, the simple laws of supply and demand dictate that the resulting construction backlog, ranging from 12 to 18 months, has increased the market price for construction services and discouraged clients and developers from commissioning new projects. Furthermore, increasing insurance premiums driven by rising replacement costs are also acting as a deterrent for new projects, particularly in the build-to-rent residential market.

When all of these factors are combined, it is no surprise that ‘high construction costs’ were frequently cited by our survey respondents as a factor in the architecture industry’s economic slowdown. “Construction costs are exceeding even the most pragmatic estimates,” the owner of a large architecture firm in Seattle told us, while the owner of a small firm in New York City explained that “Construction costs are so high that they quickly outstrip the value of a project.” Elsewhere in New York City, an architect in a large firm noted: “Clients are telling me that it is getting harder and harder to build and that costs show no sign of slowing down.”

The bottom line: The cost of running an architecture firm has risen. Rather than fees increasing in line with such costs, clients are looking to extract more services from architects for a lower price.

Our first two factors, high interest rates and construction costs, have acted to dampen the confidence of clients in commissioning new projects, thus lowering the demand for architects. At the same time, firms are grappling with higher business costs driven by inflation. In our survey, ‘inflation’ was the second-most cited reason for the industry’s economic struggles, surpassed only by high interest rates. While higher construction costs can also fall under the ‘inflation’ umbrella, architects were keen to elaborate on how inflation has impacted their own overheads and running costs, from salaries to equipment costs to utility bills.

To this end, the owner of a small firm in New Orleans cited “overhead expenses in the form of salaries, staff benefits, debt service, and consultant's fees” as the cause of their financial struggles, while an architect in a large firm in New York City told us that “overhead costs seem to be only rising.” Elsewhere, the owner of a large firm in San Francisco told us: “Inflation and business expenses are growing faster than our fees.”

From this last quote, we can extrapolate a tangential issue frequently cited within our survey: the increased cost of doing business has not been matched by an increase in the fees charged by architects and, in some cases, has resulted in fee undercutting. “Costs are up, fees are not,” the owner of a small firm in New York City told us, while the owner of a small firm in Los Angeles lamented the “other large corporate firms that undercut the competition.”

Inflation and business expenses are growing faster than our fees. — Archinect survey respondent

Several respondents noted that a stagnation or decline in fees was the result of pressures from clients. “Clients are also pushing for thinner fees from architects while demanding more work, and we, as an industry, continue to give in to the client demands,” an architect in a large New York City firm told us, while a sole practitioner in Los Angeles noted: “Clients are less likely to pay for the design intelligence that comes with hiring an architect. I'm finding that a lot of new work is looking to cut my fees by at least 50%.” Elsewhere, the owner of a small firm in New York City told us that “clients are being more information hungry on decisions, pursuing more alternates, more limited fee scopes before they pull the trigger.”

Archinect’s editorial frequently explores the longstanding struggle within the architecture profession to articulate and defend its value against other actors within the real estate sector. Responses to our survey suggest that in the current climate, as that sector looks for any and all opportunities to lower costs in response to the factors outlined in this piece, architect fees have become a target for exploitation.

The bottom line: In addition to being a major source of inflation and interest rate rises, the COVID-19 pandemic induced a shift to remote and hybrid working, which continues to suppress demand for new office space, with knock-on consequences for design services.

Despite not being explicitly identified by many of our survey respondents, the legacy of the COVID-19 pandemic looms large over our first three factors. The higher cost of construction, driven by material prices, is a clear consequence of supply chain disruption during the pandemic, as is the explosion of demand for construction services after the economy opened up from lockdowns. More broadly, the economic shock of the pandemic and financial measures taken by governments are recognized as the leading cause of inflation across the board, which itself was a driving force behind interest rate rises over the past two years. Observers looking for a simple answer to the economic turbulence of the past year may, therefore, find themselves updating the famous Clinton-era line to: “It’s the pandemic, stupid.”

Bigger corporations that did a lot of work to get people back in the office after COVID have completely backed off on doing any further work. — Archinect survey respondent

While few respondents directly attributed the pandemic to our first three factors, several respondents did identify the legacy of the pandemic-era shift to remote working as a factor behind their economic challenges, with clients particularly hesitant to commission new office projects. The owner of a mid-sized firm in Chicago observed among clients a “hesitation to spend big on space they are unsure will be used by the employee base,” while in Los Angeles, an architect in a large firm noted that “commercial real estate is failing, and return to work is weak.”

Elsewhere, an architect in a small New Jersey firm told us: “Bigger corporations that did a lot of work to get people back in the office after COVID have completely backed off on doing any further work,” before adding that clients “spent a lot of money coming out of COVID to install AV for hybrid working and install collaboration areas to support free addressing instead of traditional office and workstation ownership. Now they are cutting back on spending, because employees still aren't coming into the office.” The owner of a medium-sized firm in Irvine, CA, put it simply that clients are “standing on the sidelines until vacancy reduces.”

The bottom line: Markets hate uncertainty. In 2024, a perfect storm of instability, whose sources range from geopolitics to technology to the economic factors outlined above, has merged into a 'death by a thousand cuts' suppressing the willingness of clients to invest in multi-year projects.

The first four factors on this list represent four singular sources of economic turbulence most often cited by survey respondents. Beneath the headlines, however, were a plethora of disparate events, conditions, and controversies weighing on the minds of architects and clients alike. By themselves, such factors do not pack much of a punch in explaining the architecture industry’s economic slowdown. When combined, however, they represent an economic ‘death by a thousand cuts’; a perfect storm of instability and uncertainty depressing the willingness of developers and speculators to commit large sums to real estate design and construction.

Within our survey, these factors included wars in both Ukraine and Gaza, which have already been shown to have impacted supply chains and trade routes. Elsewhere, geopolitical tensions between the U.S. and China leave open the possibility of trade wars and goods tariffs. Within this context, one architect in a small Southwest firm told our survey that “concern about international stability is leading to some clients holding onto money.”

Against this global uncertainty, the U.S. is currently in the midst of an exceptionally tumultuous presidential election, the outcome of which may have knock-on consequences on everything from energy and labor policies to housing and infrastructure funding. Several survey respondents subsequently noted the election and government gridlock when explaining the causes of their current economic challenges.

It seems everybody is waiting for something to happen but not sure what is going to happen. — Archinect survey respondent

Artificial intelligence also plays a part in our perfect storm. Beyond the looming abstract questions about what artificial intelligence means for the future of work and the supply and demand of human labor, Archinect has heard from architects in Los Angeles who cite the recent Hollywood strikes, fuelled by fears of AI displacement, as a factor behind a decline in demands for hospitality design services. Meanwhile, Archinect previously noted how the pace of progress in AI caused Hollywood mogul Tyler Perry to pause plans for an $800 million expansion project for his Atlanta studio complex.

Above anything else, markets detest uncertainty. In 2024, the landscape presented by architects through our survey shows that there is no shortage of uncertainty and instability to fuel hesitancy among real estate developers and their investors to commit millions of dollars to years-long projects. As one architect in a small Miami firm succinctly told us: “It seems everybody is waiting for something to happen but not sure what is going to happen.”

Niall Patrick Walsh is an architect and journalist, living in Belfast, Ireland. He writes feature articles for Archinect and leads the Archinect In-Depth series. He is also a licensed architect in the UK and Ireland, having previously worked at BDP, one of the largest design + ...

23 Comments

It is not that hard to be pessimistic about architecture and everything else industry at the moment. The interest rates might never come down but go up even more. Let's be real, where do you see any substantial and sustainable growth in the economy?

Record profits for health insurance, oil and natural gas, and pharma.

Market segments of the economy that are growing: hospitality, medical, transportation, education, and construction.

No continuous growth is sustainable. Period.

It matters of course what you mean by growth. In a world of finite resources consumption of those resources cannot continue to grow, however efficiency and productivity can. But in an economy designed to aggregate those gains in the hands of just a few individuals the world will not be getting better for most people.

The population of architecture students is in decline. Private architecture schools with high tuition fees are struggling the most. Overall attendance to higher education is in decline. The hospitality industry is mainly a big service sector with service jobs.

We should aim for continuous growth in sectors that benefit the working class Americans. Developers are abandoning the multi-family housing sector for being not profitable. The growth in the transportation industry is very questionable. Those "growing" segments Chad lists are doubtful and depend on who is putting those numbers together for what purpose. And, pharma and medical industry.., puhleeze.

I'm sorry but you asked where substantial and sustainable growth were occurring in the economy. No growth is sustainable, period. The growing market segments I mentioned are directly from data from the US government and another have dozen separate economic sites. If you don't believe me go look at the economic data. Now if you had asked for market segments that are showing growth that benefited the 'working class' my answer would of been different.

What market segments are showing growth that benefited the 'working class'?

Construction. Healthcare, Education, Hospitality. All market segments that employ the working class.

I was waiting for a more intelligent answer. Not we have heard a million times from the people of corporations who are ok with these businesses that pay half a cent on the dollar to their workforce. I asked for sustainable growth not this standard "we feed our slaves" bullshit.

You asked for what market segments have shown growth that benefits the working class. Those market segments typically employ the 'working class'. As I stated previously - no growth is sustainable.

If you wanted to discuss corporate maleficence, greed, and the wadge gap you should of said so.

You talk and comprehend like Siri. It is ok but a bit like data slaving.

I'm sorry if you have trouble asking a question. Nice attempt at trolling though. Try harder next time.

Btw, I have seen the same thing in some of your other posts, accusing people of "trolling" and telling to "try harder."

Get a life!

I only do that when people are disingenuous and attempting to troll.

Look what we got here, a self-appointed neoliberal troll patrol... It would help if you looked in the mirror, Judge Judy.

For someone who's upset by being called a troll you sure do act like one. Good luck with that.

Yeah! Coming from you, I will wear my trollism as a badge of honor. I think we hijacked this thread and I wish Archinect would delete it after a few posts down when your trollist troll was trying to start some conversation that the article deserves.

Happy trollicking Judge Judy!

- Trollingo

Goodbye.

logon stop being a jerk. Chad answered what you asked and tried to have discussion and your responses have been inflammatory.

"Due to the complex nature of the financial network, only the probability of bank default is affected and not the magnitude of a money market crisis. Further, assuming that banks will try to restore business levels, raising diversification and lowering their individual risk, the dimension of the entire financial network will increase, which has the natural consequence of raising the probability of a large crisis." - 'The dynamics of financial stability in complex networks'

This is a 14-15 year old paper but very informative for an architect.

My main concern is a large financial crisis. This is especially compounded in today's political and international instability. The banking industry is the place to watch.

Here is something that might help to contextualize as it did for me.

The architecture industry would have been smart to promote accessibility and transparency of the entire construction industry to really push the idea that design leads to better outcomes in health, energy, economic wellbeing. Instead they have been pushing DEI, academic protectionism, and grasping for scraps at the kids table.

Why not both?

I wished DEI had organically occurred instead of top-down pc hiring allocations and quotas behind the doors. It would have if, "the architecture industry would have been smart to promote accessibility and transparency of the entire construction industry to really push the idea that design leads to better outcomes in health, energy, economic wellbeing." Indeed, "scraps at the kids' table" is what we have.

For Donna, I don't see this as a separate issue. I think DEI should be a nested social order in the architecture practice as described above by Chemex.

Block this user

Are you sure you want to block this user and hide all related comments throughout the site?

Archinect

This is your first comment on Archinect. Your comment will be visible once approved.